FRANKLIN ELECTRIC CO (FELE)·Q4 2025 Earnings Summary

Franklin Electric Q4 2025: Solid Execution Offsets Slight Miss, Guides 2026 Higher

February 17, 2026 · by Fintool AI Agent

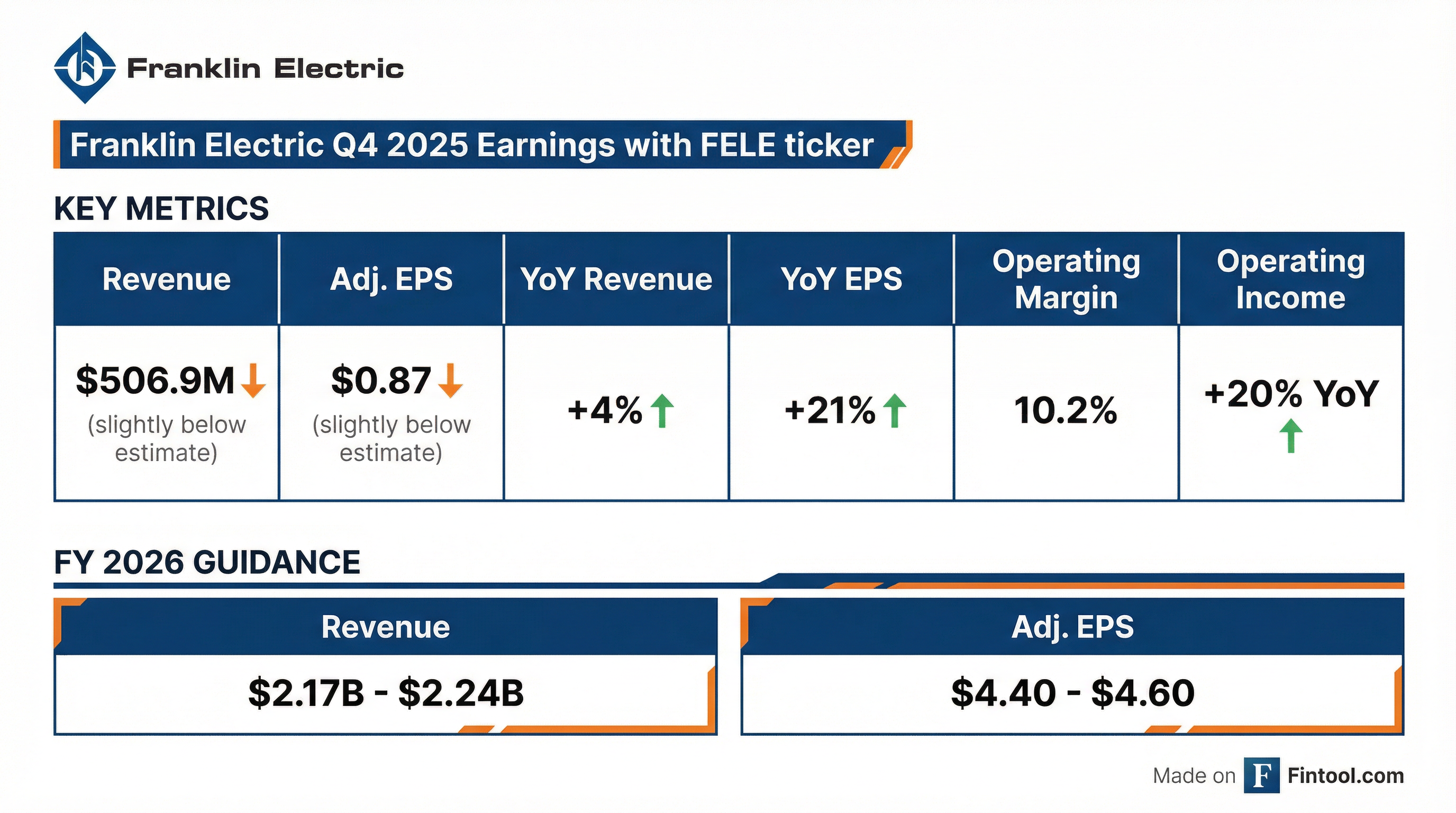

Franklin Electric (FELE) delivered Q4 2025 results that narrowly missed Wall Street expectations but showcased strong year-over-year momentum. Revenue of $506.9M came in 1.8% below consensus, while adjusted EPS of $0.87 missed by 2.5%. Despite the miss, the company posted 21% YoY EPS growth and raised FY 2026 guidance to $4.40-$4.60, signaling confidence in continued execution. CEO Joe Ruzynski noted that 2025 marked "high points for Franklin in both revenue and segment operating income."

Did Franklin Electric Beat Earnings?

Franklin Electric missed both revenue and EPS estimates for Q4 2025, though the magnitude was modest:

The miss was driven primarily by volume softness in US/Canada Water Systems (HVAC markets) and Energy Systems margin compression from international mix and tariff timing. Operating margin expanded 130 basis points to 10.2% on price, productivity, and SG&A cost management.

Beat/Miss Context: This was Franklin Electric's first miss after three consecutive quarterly beats (Q4 2024, Q2 2025, Q3 2025). The stock has run up significantly over the past year, with shares trading near 52-week highs heading into the print.

What Did Management Guide for 2026?

Franklin Electric issued FY 2026 guidance that implies continued momentum:

CFO Jennifer Wolfenbarger noted the guidance "reflects commercial and operational momentum and our commitment to continue to grow the business and expand earnings per share."

Key Guidance Drivers:

- Standard price increases passed at start of 2026 with good realization expected

- Value Acceleration Office initiatives driving productivity

- Acquisition carryover (Barnes and PumpEng closed end of Q1 2025)

- Growth expected across all quarters (normal seasonality, no back-end load)

- Beginning in 2026, guidance provided on adjusted EPS basis (excluding restructuring, one-time items)

Segment-Level Outlook:

What Changed From Last Quarter?

Improving Trends:

- Operating margin expanded to 10.2% vs 8.9% a year ago

- Distribution segment swung from near-breakeven ($0.5M operating income in Q4 2024) to $5.3M

- SG&A improved 70 bps as % of sales YoY; excluding acquisitions, SG&A down ~$3M or 3%

- Water treatment business reached $200M in sales with 400+ bps margin improvement in 2025

- Distribution business crossed $700M milestone with 210 bps margin expansion in 2025

- Energy Systems international growth +19% in Q4 (India and Europe leading)

Headwinds:

- US & Canada Water Systems revenue declined 4% on HVAC market softness

- Energy Systems Q4 margin compressed 560 bps due to geographic mix and tariff timing

- Mexico market weakness impacted Barnes integration readout

- GAAP EPS impacted by $0.91/share pension settlement charge in FY 2025

How Did the Segments Perform?

All three segments grew in Q4, with Energy Systems posting the strongest growth:

Water Systems benefited from acquisition contributions and price, though US/Canada revenue declined 4% on HVAC softness. International sales grew 15% overall. Management noted HVAC weakness was "isolated to the back end of Q4" and is "normalizing in January." Mexico market has also stabilized.

Distribution showed notable margin improvement, with operating income up from $0.5M to $5.3M YoY (300 bps expansion). Full-year operating margin expanded 210 bps to 5.7%, driven by margin enhancement initiatives and structural improvements.

Energy Systems maintained its premium margin profile at 30.3%, though margin contracted 560 bps on unfavorable geographic mix (international up 19%) and tariff timing. Management expects margins to bounce back to "mid-30s" as December price increases (1.5-2%) are realized.

Full Year 2025 Results

FY 2025 marked "high points for Franklin in both revenue and segment operating income," per CEO Joe Ruzynski:

The GAAP EPS decline reflects a one-time pension settlement charge of $41.5M after-tax, or ~$0.91/share.

How Did the Stock React?

Pre-Earnings Setup: FELE shares closed at $108.94 on February 13, 2026, trading near 52-week highs ($111.53) and well above the 50-day average of $99.78 and 200-day average of $94.41. The stock has rallied ~38% from its 52-week low of $78.87.

Earnings Release: The Q4 2025 results were released before market open on February 17, 2026. Market reaction will be reflected in today's trading session.

Historical Pattern: Franklin Electric has posted a mixed earnings record over the past 8 quarters, with beats in Q4 2024, Q2 2025, and Q3 2025, but misses in the intervening periods. The stock has generally responded positively to operational execution even when headline numbers missed slightly.

Key Management Quotes

CEO Joe Ruzynski emphasized innovation and transformation in the call:

"We had a strong Q4 and full year results in all segments. Sales were up 5.4%, and segment operating income was up 9.6% for the full year, each representing high points for Franklin in both revenue and segment operating income."

On the company's innovation pipeline:

"We believe innovation and new products are a leading indicator for growth and added over 35 products that will deliver over $160 million in revenue by year 3. We are positioning Franklin as an innovation and growth company."

On strategic positioning heading into 2026:

"We are in great businesses. As a flow control company focused on water and energy, our strategy starts with a clear view of the markets and where we can win. We see attractive markets where we can focus and grow faster."

Q&A Highlights

On 2026 Organic Growth by Segment

Management provided detailed segment expectations:

- Water Systems: 3-5% growth with a blend of acquisition carryover, volume, and price

- Energy Systems: 3%+ growth, skewing slightly more volume than price

- Distribution: 3-4% growth, roughly 50/50 price/volume split (similar to 2025)

On HVAC Weakness

The US & Canada Water Systems decline of 4% was driven by HVAC softness in the RSS business (~$150M segment). CFO Jennifer Wolfenbarger noted this was "isolated to the back end of Q4" with "normalization coming through in January." No housing recovery is assumed in guidance.

On Mexico Market

Mexican market weakness from H2 2025 "looks like it has stabilized" with rates returning to normal. This was a key integration concern for the Barnes de Colombia acquisition.

On Acquisition Integration

- PumpEng: "Ahead of track" with smooth integration. Growth synergies reading out as broader product portfolio drives new opportunities in dewatering/minerals markets.

- Barnes de Colombia: Integration progressing well but growth readout delayed due to Mexico market weakness. Stabilizing as the company exited December into January.

On Value Acceleration Office

Formalized mid-2025, this transformation initiative combines 80/20 principles, AI, and process reengineering. Key points:

- New AI director hired in Q1 2026

- Focus on scale, velocity, and growth (not just cost cutting)

- Projects already running with readout expected in 2026

- Part number normalization completed in October 2025 (aids inventory and supplier negotiations)

On 80/20 Progress

Management described 80/20 as "first three innings" for Water Systems, with opportunities in SKU rationalization across global manufacturing sites. Distribution has made "great progress" on T rationalization and spend optimization.

On Energy Margins

Q4 margin compression (560 bps YoY) was driven by two factors: strong international growth (lower margins) and tariff timing. Price increases passed in December will drive 1.5-2% realization in 2026, with margins expected to return to "mid-30s."

On 2026 Margin Outlook

- Distribution: Expected 70+ bps expansion

- Water and Energy: Slight expansion, less than Distribution

- All segments projecting growth and margin expansion

Balance Sheet and Cash Flow

Cash position declined meaningfully but remains healthy:

Capital Allocation:

- Acquisitions: ~$120M invested in 2025

- Share Repurchases: ~$160M (~1.8M shares)

- Dividends: $0.28/share quarterly dividend announced (+5.7% increase), marking 34th consecutive year of dividend increases

- Remaining buyback authorization: ~0.8M shares

Forward Catalysts

Near-Term:

- Q1 2026 earnings (typically late April)

- HVAC market recovery after Q4 weakness

- Mexico market stabilization benefiting Barnes integration

Medium-Term:

- New product launches: 35+ products expected to deliver $160M revenue by year 3

- Energy Systems: EVO and OVERSITE solutions driving above-ground product growth

- Grid business expansion with new products and channels

- Value Acceleration Office benefits reading out through 2026

- Water treatment business momentum (exited 2025 at $200M sales with 400bps margin improvement)

M&A Pipeline: Management noted the M&A market "looks to be busy this year" with focus on portfolio and channel round-outs. Balance sheet remains in "healthy leverage spot."

Risks to Watch:

- Tariff environment: December price increase passed, 1.5-2% realization expected

- Housing starts: No recovery assumed in guidance

- International mix: Strong growth but lower margins (impacted Energy Q4)

- Large dewatering cyclicality: Strong 2025, may moderate in 2026

Company Profile: Franklin Electric is a global leader in the production and marketing of systems and components for the movement of water and energy. The company serves residential, commercial, agricultural, industrial, municipal, and fueling applications across three segments: Water Systems, Distribution, and Energy Systems.

Resources: